Teeing this up for @PooPopsBaldHead

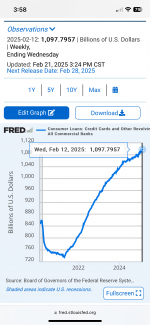

In case this requires a subscription, the jethreaux summary is that the federal government has been basically making the minimum payment for people’s mortgage while the homeowners continue to fall further behind in debt to equity. The ball is now in Orangeman’s court to continue funding it with taxpayer dollars or let it collapse and take the blame.

In case this requires a subscription, the jethreaux summary is that the federal government has been basically making the minimum payment for people’s mortgage while the homeowners continue to fall further behind in debt to equity. The ball is now in Orangeman’s court to continue funding it with taxpayer dollars or let it collapse and take the blame.